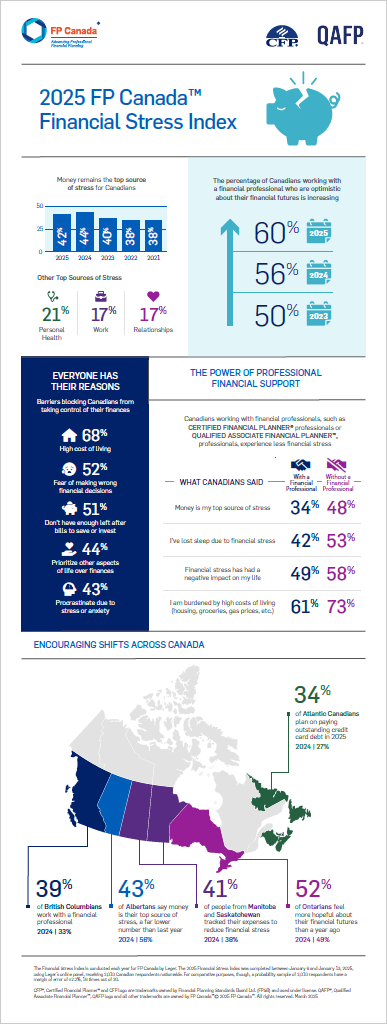

The FP Canada™ Financial Stress Index consistently finds that money is the number one source of stress for Canadians.

The good news, growing your financial literacy can help you take action that will reduce your financial stress. By turning to a professional financial planner, you can take a critical first step toward becoming more financially literate.

A Certified Financial Planner® professional or Qualified Associate Financial Planner™ professional can help educate you on financial matters. They can also provide you with the tools to stay on top of basics like budgeting, retirement planning, saving, and debt reduction.

Let’s run through some of the financial planning basics with the help of Stacy Whytewood, a CFP® professional in Moncton, N.B., and Kevin Cork, a CFP professional in Calgary.

Budgeting

This is a core component of financial planning.

“It’s hard to overstate the importance of a budget when you’re first trying to get a handle on your money,” says Whytewood.

“A budget or spending plan is a road map that gives you directions every month on how to allocate your money. At its most rudimentary, a budget lists how much income you have coming in compared to what's going out each month. But creating a more detailed budget—either online, on paper or via a host of handy budgeting apps that you can download onto your smartphone—allows you to make smarter decisions about your finances each and every day.”

When you're tempted to spend money on something, a budget will encourage you to give the potential purchase a second thought. You’ll often realize that if you give into that temptation to spend, you won’t be able to spend or save elsewhere.

And at the end of every month, if you have some surplus, you can put it towards your savings or paying down debt.

One of the most important steps in getting out of debt is to pay more than the minimum amount due each month, because even a relatively modest credit card balance can take years to pay off if you’re only paying the minimum amount due to interest and finance charges,” says Whytewood

Reducing Expenses

After you've successfully created a budget, you'll see where your money is going and where you can cut back on spending. For some, it can also mean comfortably spending a little more and not feeling guilty.

“For most people, it’s as simple as trimming your expenses on little things, like recurring memberships for services you rarely use or going out for drinks or dinner two less times a month,” says Cork.

“Or it may require making deeper permanent changes to your lifestyle, like refinancing your mortgage, renegotiating your rent or entirely eliminating expenditures like dining out or travelling until you get a firmer handle on your finances.”

That way, you can pay down debt faster, build up an emergency fund or contribute to your retirement savings. And once one debt is paid off, immediately redirecting most of that money to another debt (or to your RRSP) is a painless way to amplify your progress without feeling any extra pinch.

Debt Reduction

Even after creating a budget, sticking to it, and cutting unnecessary expenses, debt may still be an issue. Most of us carry some, but there’s a big difference between mortgage debt and credit-card debt. Tackling the debt with the highest interest rates must be the top priority.

“Getting out of debt becomes extremely difficult when you're facing sky-high interest rates on credit cards or loans,” Whytewood points out. “One of the most important steps in getting out of debt is paying more than the minimum amount due each month, because even a relatively modest credit card balance can take years to pay off if you’re only paying the minimum amount due to interest and finance charges.”

Those charges could end up costing you thousands of dollars that could have gone towards your savings.

Options to help reduce credit-card debt can include a debt consolidation with a loan or line of credit. You could also do a balance transfer to a new card that will waive interest payments for an initial period of time, Whytewood says. If you don’t have to pay interest for a year, that gives you time to make a big dent in repayment.

Retirement Planning

With fewer companies offering pension plans, it's more important than ever to save and plan for your retirement via RRSPs and tax-free savings accounts (TFSAs).

“Retirement savings should be a priority, not an afterthought,” says Cork. “If you're not saving for retirement yet, revisit your budget to see if you have room to include it.”

The earlier in the year you invest in an RRSP or TFSA, the sooner your money can start growing—and the sooner it’s protected from taxation. In other words, don’t wait for the deadline.

And you can sign up for an automatic savings plan for both your RRSP and TFSA. This step will make it easier to save and maximize your opportunity for returns.

Money stresses many Canadians out, but it doesn’t have to. Take the time to tackle these four basics, and you’ll soon be well on your way to financial well-being. Begin by finding a CFP professional or QAFP® professional near you with our Find Your Planner tool.